Weekly Mortgage & Market Update

Week of November 17, 2025

This week brought a mix of signals about the economy: stronger-than-expected job growth, a rising unemployment rate, improving home sales, and slightly better builder confidence. With the Fed’s next meeting just weeks away, these numbers matter. Our goal is to break them down clearly so you know what actually impacts mortgage rates, affordability, and the broader housing market.

Will the September Jobs Report Lead to a Fed Pause

After delays caused by the government shutdown, the September Jobs Report finally arrived — and it came in stronger than economists expected. Employers added 119,000 jobs versus the forecast of 50,000. However, revisions to July and August softened that headline, with August ultimately showing a decline of 4,000 jobs. June also saw a loss of 13,000 jobs. These are the first back-to-back monthly job declines since December 2020.

The unemployment rate inched up from 4.3% to 4.4%, showing signs of cooling beneath the surface.

One thing the timing affects: the Bureau of Labor Statistics will release only partial October data (without an unemployment rate) alongside the full November report on December 16 — well after the Fed’s December 9–10 meeting. That means the Fed will make its next decision without a clean October jobs report.

The Fed has already cut the Federal Funds Rate in September and October as it tries to balance high inflation with signs of a cooling job market. But Chair Jerome Powell continues to emphasize that there’s “no risk-free path” and that another rate cut is “not a foregone conclusion.” Meeting minutes show real division inside the Fed, and recent speeches only confirm that policymakers remain split.

The tension comes down to this: high inflation argues against cutting rates, while weakening labor data argues for easing. With September showing stronger job growth but a rising unemployment rate — and no more BLS jobs reports before the December meeting — the odds of another cut remain uncertain.

Quick refresher: when the Fed changes rates, it adjusts the Federal Funds Rate. That does not directly set mortgage rates, but it influences them through economic expectations, bond markets, and inflation trends.

Jobless Claims Data Signals Slower Hiring

Now that the BLS has released the backlog of jobless claims, we can also see what happened in recent weeks. Initial Claims held between 220,000 and 235,000 through October and November. Continuing Claims — which reflect people who remain on unemployment benefits — stayed above 1.9 million each week, with the latest reading at 1.974 million.

Relatively low initial claims mean layoffs aren’t spiking, which is good. But continuing claims staying above 1.9 million since mid-May tells us people are taking longer to find new jobs. That’s a clear sign of a cooling labor market.

October Existing Home Sales Rise Again

The National Association of REALTORS® reported that existing home sales rose 1.2% from September to October and were 1.7% higher than a year ago. Inventory dipped to 1.52 million units but remained almost 11% above last year’s level.

Because October closings reflect buyer decisions made in August and September, this report only captures the early part of the recent rate declines. We may see even stronger sales in upcoming reports.

NAR Chief Economist Lawrence Yun said it clearly: “Home sales increased in October even with the government shutdown due to homebuyers taking advantage of lower mortgage rates.”

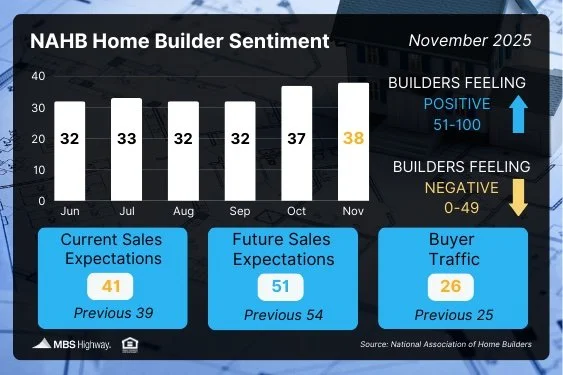

Home Builder Confidence Inches Higher

Builder sentiment rose one point to 38 in November — the best reading since April — according to the National Association of Home Builders. This beat expectations for no change.

Buyer traffic improved to 26. Current sales conditions rose to 41. Expectations for future sales dipped three points to 51 but remained above the key 50 threshold for the second straight month.

Uncertainty remains, but easing mortgage rates are improving affordability. NAHB Chief Economist Robert Dietz noted that the organization expects a modest uptick in single-family construction next year.

Home Life Tip of the Week

With National French Toast Day and Black Friday landing on the same date this year (November 28), here’s a perfect long-weekend breakfast from Food & Wine. Serves 4.

In a shallow dish, whisk together 3 extra-large eggs, 1/2 cup milk, 1/2 teaspoon vanilla, 1/2 teaspoon cinnamon, and a pinch of nutmeg. Dip four 3/4-inch slices of challah bread into the mixture, turning to coat evenly.

Melt 2 1/2 tablespoons butter in a large skillet over medium-low heat. Add two slices and cook for about 2 minutes per side, until golden brown. Repeat with the remaining slices. Serve warm with maple syrup — or elevate it with berries, powdered sugar, or whipped cream.

What to Look for This Week

Tuesday brings delayed September data on wholesale inflation and retail sales. We’ll also get new reports on home price appreciation from Case-Shiller and the FHFA, plus the latest Pending Home Sales numbers from the NAR.

Technical Picture

Mortgage Bonds finished last week testing a dual ceiling of resistance at their 50-day and 25-day Moving Averages. A break above those levels could open roughly 40 basis points of additional upside before the next strong resistance near 101.44.

The 10-year Treasury yield moved below its 50-day moving average and ended the week testing the 25-day. If yields fall below that, the next target is 4%.

Source: MBSHighway